When GPs ask us, “What’s the best entity structure for a real estate fund?” they usually mean the fund entity itself. Should it be an LLC or a limited partnership?

That’s the wrong question. Or at least, it’s an incomplete one.

Your fund isn’t one entity. It’s a stack of entities, and each one serves a specific purpose: liability isolation, tax efficiency, fee separation, and operational clarity. Getting any single entity wrong can create tax problems, accounting headaches, or governance issues that follow you for the life of the fund.

We covered the LLC vs. LP comparison for the fund entity itself in a separate post. This one goes wider. Here’s the full picture of how a real estate fund’s entity structure should work, from the fund down to the individual properties, and why each piece matters from a tax and accounting perspective.

The Standard Four-Entity Stack

Most well-structured real estate funds have four layers of entities. Each one exists for a reason.

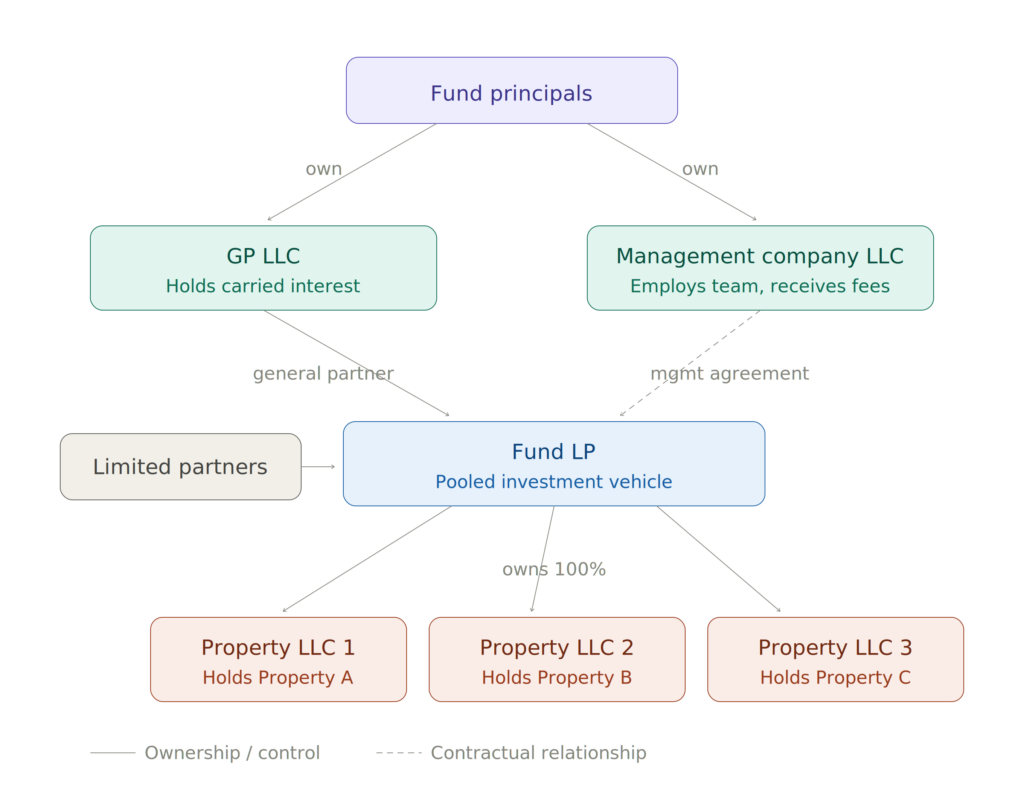

1. The Fund Entity

This is the pooled investment vehicle. Investors commit capital here. The fund holds equity interests in subsidiary entities that own the properties.

Most funds are structured as either a Delaware limited partnership (LP) or a manager-managed LLC. We wrote an in-depth comparison of the two, but the summary:

- LP if you’re raising from institutional investors, want clean self-employment tax treatment for LPs, and value decades of Delaware case law.

- Manager-managed LLC if you want simpler formation, fewer entities, and more governance flexibility.

The fund entity files Form 1065 and issues K-1s to every investor. It’s the entity your LPs interact with and the one your CPA spends the most time on.

2. The General Partner Entity

The GP entity manages the fund and holds the carried interest (promote). It’s typically an LLC owned by the fund’s principals.

Why a separate entity? Three reasons.

Liability protection. In an LP structure, the general partner has unlimited liability. If the GP is an LLC rather than an individual, personal assets are shielded behind the LLC.

Carried interest separation. The GP entity’s carried interest is a profits interest in the fund. Keeping it in a dedicated entity makes it easier to track promote allocations, manage GP co-invest capital, and separate carried interest income from management fee income for tax purposes.

Flexibility for GP economics. If you have multiple principals sharing the promote, the GP LLC’s operating agreement defines how the carry splits between them. This is a private arrangement that doesn’t need to involve the LPs or the fund’s governing documents.

The GP entity is usually a simple LLC. It files its own Form 1065 (if it has multiple members) or is a disregarded entity (if single-member) that flows through to the owner’s personal return.

3. The Management Company

The management company (ManCo) employs the team, pays salaries, and receives the management fee from the fund. It’s a separate entity from both the fund and the GP.

This is the entity most first-time fund managers skip or combine with the GP. Don’t.

Here’s why the separation matters:

Tax character of income. Management fees are ordinary income subject to self-employment tax. Carried interest income can qualify for capital gains treatment. If the GP entity receives both the management fee and the carry, it creates commingling risk. The IRS could argue that some of the carry is really disguised compensation for services, or that expenses are being misallocated between the two income streams.

Management fee waivers. If you’re using a fee waiver strategy (waiving the management fee in exchange for an increased profits interest), having the ManCo and GP as separate entities makes the arrangement cleaner. The ManCo waives its fee. The GP’s profits interest increases. The two streams never touch.

Scalability. If you launch Fund II and Fund III, the same ManCo can service all funds. It signs a management agreement with each fund and invoices each one for fees. The GP entity, on the other hand, is typically specific to each fund (Fund I GP LLC, Fund II GP LLC, etc.) because each fund’s carry is a different economic arrangement.

Employment and operations. Payroll, health insurance, office leases, and operating expenses live in the ManCo. Keeping these out of the fund entity keeps the fund’s books clean and prevents fund-level expenses from getting tangled with operating overhead.

The ManCo can be structured as an LLC (most common), an S-corp (if self-employment tax savings justify the complexity), or a C-corp (rare, but sometimes used for certain benefits or international investors).

4. Property-Level LLCs (SPVs)

Each property the fund acquires should generally be held in its own special purpose vehicle (SPV), typically a single-member LLC owned by the fund.

Why one LLC per property?

Liability isolation. If a tenant lawsuit, environmental issue, or lender default occurs at one property, the liability is contained within that property’s LLC. It doesn’t affect the fund’s other assets.

Financing flexibility. Lenders typically require a single-asset entity for each mortgage. This is standard in commercial real estate lending.

Exit flexibility. When the fund sells a property, it can sell the asset out of the LLC or sell the LLC itself (an “entity sale”). Each approach has different tax consequences. Having a clean, single-asset entity gives you both options.

Co-investor accommodation. If the fund brings in a property-level co-investor or JV partner on a specific deal, the property LLC can accommodate that structure without affecting the fund’s other investments.

Clean accounting. Each property LLC has its own bank account, its own P&L, and its own books. This makes property-level reporting straightforward and investor reports more accurate.

Property-level LLCs are almost always single-member LLCs owned by the fund. As disregarded entities for tax purposes, they don’t file their own tax returns. Their income and expenses flow up to the fund’s Form 1065.

Visualizing the Full Structure

Here’s what the standard entity stack looks like:

Fund Principals (Individuals) ↓ own GP LLC (holds carried interest, manages the fund) ↓ serves as general partner of Fund LP (the pooled investment vehicle; LPs invest here) ↓ owns 100% of Property LLC 1 → holds Property A Property LLC 2 → holds Property B Property LLC 3 → holds Property C

Fund Principals (Individuals) ↓ also own Management Company LLC (employs team, receives management fees from the Fund)

The fund has a management agreement with the ManCo. The GP has a partnership agreement with the fund (the LPA). Each property LLC has an operating agreement and a deed.

Common Structural Mistakes

We’ve seen all of these. Each one creates problems that are expensive to fix after the fact.

Combining the GP and ManCo

This is the most common mistake. The GP entity receives both the management fee and the carried interest. This muddies the tax treatment, complicates fee waiver strategies, and creates allocation issues when preparing K-1s.

Fix: form a separate ManCo before the fund’s first capital call. It costs a few hundred dollars and saves thousands in accounting and tax complications.

Using One LLC for Multiple Properties

Some GPs put two or three properties into a single LLC to save on formation costs. This eliminates liability isolation. If one property has a problem, creditors can reach the equity in the other properties held in the same entity.

Fix: one LLC per property. Formation costs are minimal ($100-$500 per state) relative to the protection they provide.

Forming Everything in the Fund’s Home State

A GP in Texas forms all entities in Texas, even though the fund is raising capital nationally and properties are in five different states. Texas may not be the best jurisdiction for the fund entity, the GP, or the ManCo.

Most funds form the fund entity and GP entity in Delaware because of its well-developed partnership law, business-friendly courts (the Court of Chancery), and predictable legal framework. Property LLCs are typically formed in the state where the property is located.

Fix: form the fund and GP in Delaware. Form property LLCs in the state where each property sits. Register as a foreign entity in states where you’re doing business.

No Operating Agreement for the GP Entity

The GP LLC was formed in a rush. The attorney filed the articles but never drafted an operating agreement. The principals assume they’ll “figure it out later.”

Then a dispute arises about how the promote splits between the principals. Without a written agreement, there’s no clear answer.

Fix: every entity in the stack needs a governing document. The GP LLC operating agreement should define ownership percentages, promote splits between principals, decision-making authority, and what happens if a principal leaves.

Skipping the ManCo for Fund I and Adding It for Fund II

Some GPs run Fund I without a ManCo, realize the mistake, and create one for Fund II. Now they have two funds with different entity structures, different fee flow mechanics, and different accounting setups. The ManCo has to invoice one fund but not the other.

Fix: build the full four-entity stack from the start, even for Fund I. The marginal cost is trivial. The structural consistency is invaluable as you scale.

Advanced Structural Considerations

For larger or more complex funds, the standard four-entity stack may need additional layers.

Blocker Entities

Tax-exempt investors (foundations, endowments, pension funds) and foreign investors may need a “blocker” entity between themselves and the fund. The blocker is typically a C-corporation that invests in the fund on behalf of the investor.

Why? Tax-exempt investors face Unrelated Business Taxable Income (UBTI) when they invest directly in a partnership that uses debt financing (which most real estate funds do). Debt-financed income creates UBTI, which triggers tax for an otherwise tax-exempt entity.

A blocker corporation absorbs the UBTI at the corporate level, and the tax-exempt investor receives dividends from the blocker instead. The trade-off is corporate-level tax on the blocker’s income, but for many institutional investors, this is preferable to UBTI complications.

If you’re raising from institutional investors, discuss blocker structures with your attorney and CPA during fund formation.

Parallel Funds

Some fund managers create parallel fund vehicles to accommodate different investor types. A domestic fund for U.S. investors and an offshore fund (often Cayman Islands) for foreign investors. Both funds invest side-by-side in the same deals, but the offshore vehicle addresses withholding tax and FIRPTA concerns for non-U.S. investors.

This adds significant accounting complexity. You’re maintaining two sets of books, two sets of capital accounts, and two sets of K-1 equivalents. Only pursue this if your investor base justifies it.

Holding Company Layer

Some funds add a holding company LLC between the fund and its property-level SPVs. This creates an additional layer of liability isolation and can simplify certain lending arrangements where the lender wants a single borrower entity that holds equity in multiple properties.

The trade-off is additional entity maintenance, bank accounts, and accounting overhead. Weigh the benefits against the complexity.

How Entity Structure Affects Your Accounting

Every entity in your structure creates accounting work. Each one needs:

- An EIN

- A bank account

- A chart of accounts

- Monthly book entries

- Intercompany transaction tracking

- Year-end tax compliance (or flow-through reporting for disregarded entities)

A fund with four properties has at minimum seven entities (fund, GP, ManCo, four property LLCs). That’s seven bank accounts to reconcile, intercompany balances to track across seven entities, and a consolidated view to produce for investor reporting.

This is why fund accounting is fundamentally different from property-level bookkeeping. And it’s why the entity structure should be designed with accounting in mind, not just legal protection.

The best time to involve your CPA in the entity structure discussion is before formation. Your attorney designs the legal framework. Your CPA makes sure the framework can be maintained operationally and doesn’t create unnecessary tax inefficiencies.

The Right Structure Depends on Where You’re Going

A GP launching a $5 million Fund I with 10 individual investors needs the standard four-entity stack. That’s sufficient, clean, and affordable.

A GP launching a $50 million Fund III with institutional LPs, a fee waiver strategy, properties in eight states, and blocker entity requirements needs a more complex structure. But it should still be built on the same foundation.

The smartest approach is to build the standard four-entity stack correctly from day one and add complexity only when a specific investor type, deal structure, or tax strategy requires it. Don’t over-engineer Fund I. But don’t under-engineer it either.

Planning your fund’s entity structure? Reach out to us and we’ll work with your attorney to make sure the structure works from a tax and accounting perspective before you file a single document.